10 min read

BE (NYSE) | ~$140 | 1-Year: $225+ | 5-Year: $600+

By Ben Pouladian

AI, semiconductors, software, and public-market research

BE (NYSE) | ~$140 | 1-Year: $225+ | 5-Year: $600+

By Ben Pouladian

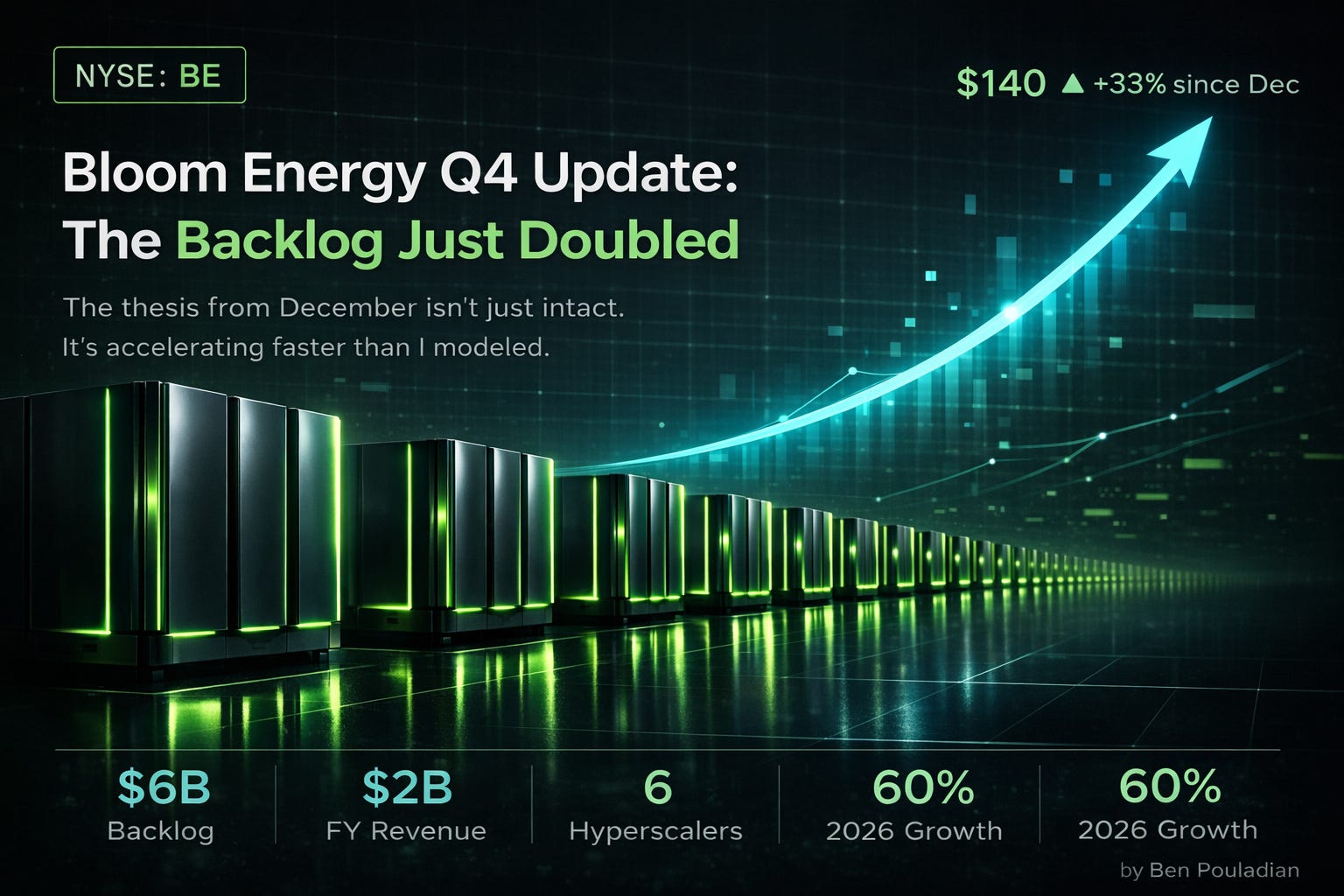

Happy Friday. What a week! So much stuff happens in the AI world its hard to keep up. Two months ago, I published “Bloom Energy Is Actually Getting Deployed” when the stock was around $105. The thesis was simple: Wall Street was treating Bloom like a concept stock while permits were being filed and hyperscalers were signing real contracts. The stock is up roughly 33% since then. But more importantly, every metric I was tracking has improved—some dramatically.

Bloom just reported Q4 and full-year 2025 results yestarday. Let me walk through what matters.

Q4 revenue came in at $777.7 million, up 35.9% year-over-year. Full-year 2025 revenue hit $2 billion, up 37.3%. Both crushed expectations.

But the headline number is the product backlog: $6 billion. That’s up 140% year-over-year, more than doubled from $2.5 billion at year-end 2024. When I wrote the December piece, the backlog was already strong. It just got dramatically stronger.

Add $14 billion in service backlog—with a 100% service attach rate on every new order—and you’re looking at $20 billion in total contracted business for a company that just did $2 billion in revenue. That ratio tells you something about the growth trajectory ahead.

A few other highlights from the quarter:

Non-GAAP gross margin: 31.9% in Q4, 30.3% for the full year (up from 28.7% in 2024)

Adjusted EBITDA: $271.6 million for the year—proving real operating leverage

Service gross margin hit 20% in Q4—eight consecutive profitable quarters

Balance sheet: $2.5 billion in total cash

Free cash flow positive for the second consecutive year

Management guided 2026 revenue of $3.1 billion to $3.3 billion—roughly 60% growth at the midpoint. Non-GAAP gross margin of approximately 32%. Non-GAAP operating income of $425 million to $475 million.

Let that operating income number sink in. In my December piece, I was modeling roughly $8 in 2027 EPS. The 2026 operating income guidance of $450 million at the midpoint, combined with approximately $1.40 in non-GAAP EPS for this year alone, confirms the earnings ramp is tracking ahead of where I expected.

The guide implies Bloom will more than double operating profit year-over-year, on top of 60% revenue growth, while expanding margins. That’s the operating leverage story playing out in real time.

This is the stat from the call that stopped me cold. K.R. Sridhar disclosed that the $6 billion product backlog now includes six hyperscale and neocloud end customers. A year ago, it was one.

He didn’t name them all. But we know the roster includes Oracle, AEP (serving hyperscaler end customers), Brookfield, and Crusoe. The master contract structure Bloom has built means these customers can return for repeat orders without renegotiating from scratch—the same model that’s driven two-thirds of their commercial and industrial revenue from repeat customers year after year.

The AEP relationship deserves special attention. The $2.65 billion order—the largest in Bloom’s history—is now characterized as unconditional. AEP will take delivery of the fuel cells regardless of downstream offtake finalization, which management says is expected in Q2. AEP reports earnings on February 12, which should provide more color on the counterparty and deployment timeline.

Here’s a data point that reframes the entire competitive narrative. Two years ago, over 80% of Bloom’s US backlog was in California and the Northeast—high-electricity-cost states where fuel cells had an obvious economic edge. Today, over 80% of the backlog comes from other states with lower power costs.

This is significant because it demolishes the bear argument that Bloom only works where electricity is expensive. Companies are building factories and data centers in states with robust natural gas infrastructure and favorable on-site power regulations. Bloom is winning on speed, reliability, and total value proposition—not just on electricity cost arbitrage.

When K.R. says “irrespective of gas prices, irrespective of utility prices, we are able to compete,” the backlog data backs it up.

In December, I identified the 800V DC architecture as Bloom’s “real unlock”—the native alignment with where NVIDIA is taking datacenter power delivery. On this call, K.R. moved it from roadmap to reality.

Starting now, every Bloom server ships 800V DC-ready with a removable adapter that lets customers deploy in legacy AC environments and migrate to DC on their own timeline. Every previously shipped server can be retrofitted for backward compatibility.

K.R. was emphatic: “800 volts DC will soon be the data center standard because physics requires it.” Any datacenter using grid, turbines, or engines will need transformers, rectifiers, and power conditioning equipment to convert high-voltage AC to 800V DC. “Bloom, and only Bloom, natively produces 800 volts DC today. No Band-Aids or adapters needed.”

The Jefferies report noted that investor enthusiasm has surged in Asia, with Bloom now being compared to HVDC-adjacent names—a signal that the market is beginning to assign structural value to this architectural advantage.

The earnings call revealed two technical capabilities that make Bloom’s value proposition wider than I’d captured in December.

Load following without batteries. Bloom’s solid-state platform can track AI workload power swings in real time—millisecond response—without requiring battery banks. K.R. called this “huge.” It eliminates an entire supply chain constraint (batteries), removes fire hazard risk, and cuts cost. Combined-cycle gas turbines, with their mechanical inertia, cannot follow load at this speed. They need batteries as band-aids.

Absorption cooling from waste heat. Because Bloom generates power on-site, the high-quality waste heat can drive absorption chillers for datacenter cooling. Management claims this can reduce datacenter electricity consumption by 20% or more. Traditional datacenters can’t do this because their power is generated hundreds of miles away. This is another “app on the platform” that has no equivalent from legacy power suppliers.

Both of these capabilities widen the moat and make it harder to compare Bloom’s total cost of ownership against simpler $/kW metrics for turbines.

K.R. made a point of noting what happened in the 48 hours around Bloom’s earnings call. Amazon announced $200 billion in 2026 CapEx—nearly doubling year-over-year. Google guided $175 billion to $185 billion. Both primarily for AI and digital infrastructure.

“Everything is digital. This is digital infrastructure. Digital runs on electricity. Electricity at that pace cannot be delivered by anyone in the free world today using poles and wires.”

The hyperscalers are spending nearly $700 billion this year on infrastructure, and the binding constraint is still power. This is the secular tailwind that makes Bloom’s backlog growth sustainable, not cyclical.

The stock opened up 12% on February 6 and gave back most of those gains intraday. Why?

Jefferies, which has an Underperform rating and a $92 price target, published their flash note identifying the key concern: Bloom didn’t announce incremental capacity expansion. The backlog doubled, but management didn’t commit to specific new manufacturing capacity beyond the previously announced ramp to 2GW. Jefferies flagged that the cadence of backlog-to-revenue conversion “could be more elongated” and said they “came away with more questions than answers.”

The Motley Fool highlighted margin compression—Q4 gross margin of 31.9% was down from 39.3% in Q4 2024, and on a GAAP basis, Bloom was roughly breakeven for the quarter and lost $0.37 per share for the full year. At ~$140 per share with non-GAAP EPS of approximately $1.40 guided for 2026, the stock trades at 100x forward earnings.

These are legitimate concerns. The valuation is rich. The GAAP profitability is thin. And the capacity expansion question matters—you can’t convert a $6 billion backlog on 2GW of manufacturing capacity without expanding further.

But here’s K.R.’s response, and I think it’s the right framework: “Capacity expansion requires a significantly lower upfront investment, a fraction of what legacy players need. Our return on invested capital for capacity expansion is a few months, not years.” He explicitly said Bloom will “continuously keep expanding” capacity as demand requires it. The reason they didn’t announce a big expansion isn’t hesitation—it’s that their model doesn’t require locking in massive capital years ahead. They can ramp in months.

The bears are measuring Bloom with industrial-age metrics. The company is running a tech-style, asset-light manufacturing model.

My December targets were $200+ one-year and $600+ five-year at a ~$105 entry. With the stock now at ~$140 and the fundamental picture stronger, I’m adjusting slightly.

The 2026 operating income guide of $425M-$475M implies approximately $1.40 in non-GAAP EPS. If Bloom sustains 30%+ revenue growth into 2027 (which the $6 billion backlog supports), 2027 EPS could reach $3-4 as margins expand and operating leverage compounds. By 2028, if the backlog conversion plays out and 800V DC becomes the standard architecture, $6-8 in EPS is achievable.

At 30x 2028 EPS of $7, you get a $210 stock. At 35x, you get $245. For a company growing revenue 40-60% annually with expanding margins, those multiples are reasonable.

Not financial advice. Do your own research.

Updated Targets:

1-Year (YE 2026): $225+

5-Year Upside: $600+

Downside Risk: $80-100 (higher floor than December given backlog confirmation)

The five-year target is unchanged. If Bloom captures a meaningful share of the behind-the-meter AI power market and the 800V DC architecture becomes industry standard, the earnings power of this business is enormous. The near-term target moved up because the backlog and guidance removed significant execution risk from the 2026-2027 trajectory.

February 12: AEP earnings. This is the most important near-term catalyst. AEP’s commentary on the Bloom order—and potentially the identity of the hyperscaler counterparty—will either validate or complicate the backlog conversion thesis.

Oracle warrant details. K.R. confirmed the strategic partnership agreement hasn’t been finalized yet, but said details are forthcoming. The warrants were struck at market prices, not penny warrants. The commercial relationship is active “across many projects.”

Brookfield Europe deployment. The first European deployment was expected before year-end 2025. Any update on international traction matters for the long-term story.

Capacity expansion announcements. Jefferies is right that this is the key conversion question. I expect Bloom will announce expansion when specific large orders require it, not on an arbitrary timeline.

In December, my thesis was that Bloom was getting deployed and the market hadn’t caught on. Two months later, the product backlog has doubled to $6 billion. The customer count went from one hyperscaler to six. Revenue guidance of $3.2 billion for 2026 represents 60% growth. Every new server ships 800V DC-ready. And the hyperscalers just committed nearly $400 billion to 2026 infrastructure spending.

The stock is up 33% from my initial write-up, but the fundamental story has improved by more than the stock price reflects. The backlog-to-market-cap ratio is more favorable now than it was in December.

Is it expensive on trailing metrics? Absolutely. Is it a concept stock? Not anymore. Not with $6 billion in orders and $2 billion in annual revenue.

I remain long and continue to see this as one of the best risk/rewards in AI infrastructure.

Ben Pouladian is a Los Angeles-based tech investor and entrepreneur focused on AI infrastructure, semiconductors, and the power systems enabling the next generation of compute. He was co-founder of Deco Lighting (2005–2019), where he helped build one of the leading commercial LED lighting manufacturers in North America. Ben holds an electrical engineering degree from UC San Diego, where he worked in Professor Fainman’s ultrafast nanoscale optics lab on silicon photonics and micro-ring resonators, and interned at Cymer, the company that manufactures the EUV light sources for ASML’s lithography systems.

Follow on Twitter/X: @benitoz | More at benpouladian.com

Disclosure: I hold a position in BE. This is investment research, not advice. Do your own work.

Originally published on BEP Research on Substack. Subscribe for more.

Leave a Reply