10 min read

.

AI, semiconductors, software, and public-market research

Micron reported earnings today (December 17, 2025) and the numbers are staggering: $13.64 billion in revenue (up 57% YoY), $4.78 non-GAAP EPS (crushing consensus of ~$3.96), and a 56.8% gross margin that expanded 11 percentage points sequentially. For context, this is the third consecutive quarter of record revenue.

But it’s the Q2 guidance that truly stunned the street: $18.7 billion in revenue and $8.19 EPS—guidance that, as Morgan Stanley noted, represents “likely the best revenue/net income upside in the history of the US semis industry, with revenue guidance $3.7 billion above consensus and net income guidance 75% above.”

The stock is up 10% after hours. But I want to dig into something more interesting than the numbers themselves: the debate playing out in real-time about whether this cycle is different.

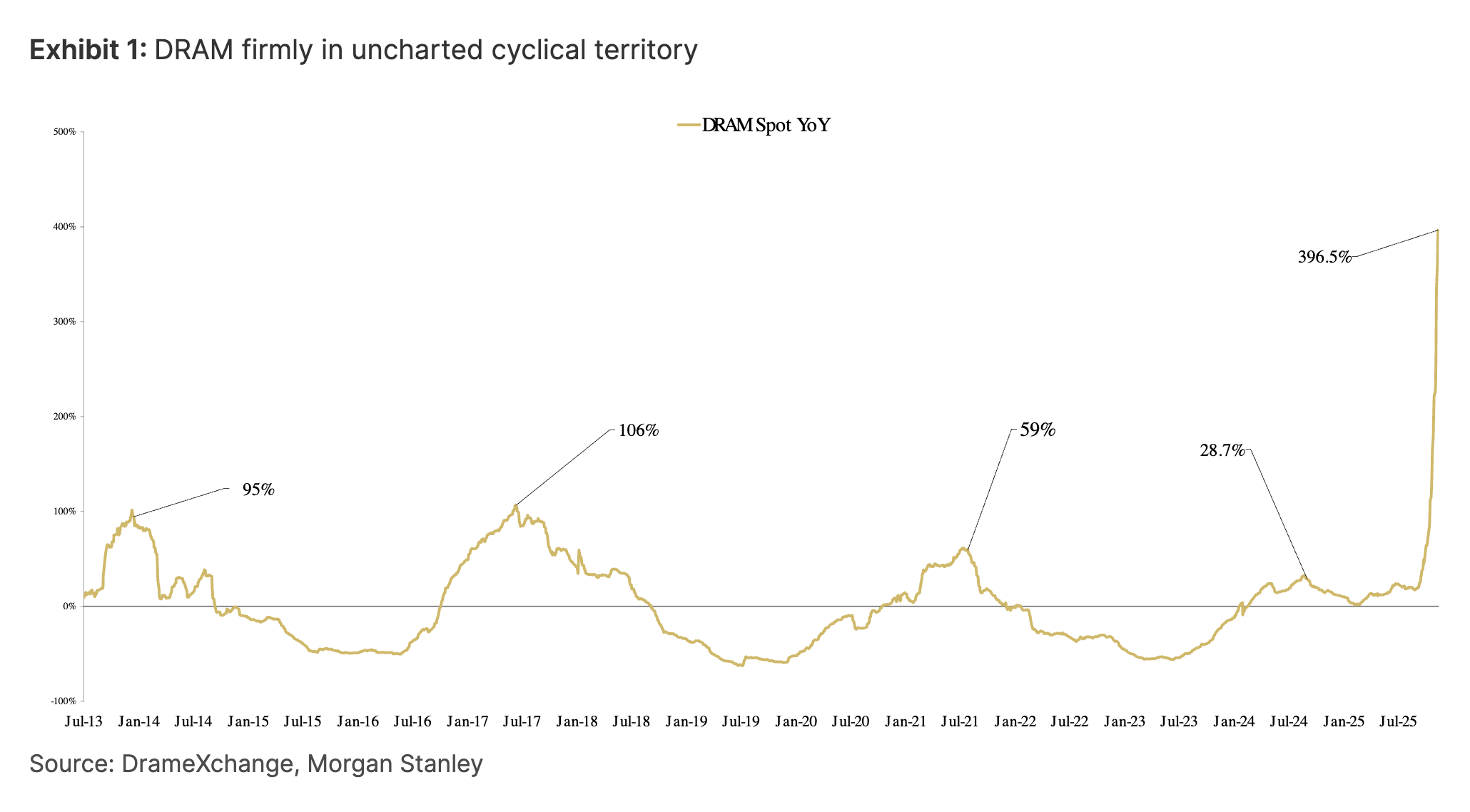

DRAM spot prices YoY — we’re in uncharted territory. (Source: DRAMeXchange, Morgan Stanley)

Let’s break down what Micron actually delivered:

DRAM: $10.8 billion in revenue (a record), up 69% YoY. Bit shipments were up slightly, but prices rose 20% sequentially. That’s pricing power you don’t typically see in commodity memory.

HBM: The high-bandwidth memory story continues to accelerate. Micron now expects the HBM total addressable market to hit $100 billion by 2028—up from $35 billion in 2025. Critically, that $100 billion milestone is arriving two years earlier than their prior outlook. CEO Sanjay Mehrotra noted: “Remarkably, this 2028 HBM TAM projection is larger than the size of the entire DRAM market in calendar 2024.”

Data Center Dominance: Server unit demand has strengthened dramatically—Micron now expects high-teens percentage growth in 2025, up from their prior 10% outlook. The AI infrastructure buildout is accelerating, not decelerating.

Crucial Exit: Earlier this month, Micron announced it’s exiting the Crucial consumer business entirely. This is strategic focus in action—they’re betting the farm on enterprise and AI.

And the DRAM spot market? Year-over-year pricing is up nearly 400%—uncharted territory in memory industry history.

When I worked in silicon photonics at UCSD, studying micro-ring resonators in Professor Fainman’s lab, I learned that paradigm shifts in physics happen slowly—then suddenly. The memory market feels similar right now.

Here’s what the bulls see:

Structural demand shift: AI has fundamentally changed memory economics. Memory content per AI server runs 5-294x higher than traditional servers. The hyperscalers aren’t just buying more—they’re buying qualitatively different products (HBM3E, LP5, DDR5) that command premium pricing.

Supply discipline: The oligopoly has learned. Samsung, SK Hynix, and Micron aren’t racing to add capacity like they did in previous cycles. New fabs won’t relieve constraints until 2027-2028 at the earliest. On today’s call, Mehrotra was emphatic: “2026 supply on each PM will be tight. HBM DRAM will be tight as well… we are continuing to see a tightening supply environment.” He added that as customer architectures evolve across AI platforms, they’re requiring more and more HBM—memory has become “critical” to delivering AI capabilities.

HBM isn’t commodity DRAM: This is crucial. HBM requires through-silicon via technology, advanced 3D stacking, and integration with logic base dies. Qualification cycles with customers like NVIDIA run 6-12 months. HBM4E will introduce customized logic dies manufactured at TSMC—transforming memory from a standard product into semi-custom silicon. That’s a moat.

The numbers: Micron’s gross margin just hit 56.8% and they’re guiding to 67% next quarter. Free cash flow was $3.9 billion—a quarterly record exceeding their prior peak from 2018 by over 20%. This isn’t a cyclical blip; it’s a fundamental repricing of memory’s value in the AI stack.

I had a conversation recently with some sharp traders who laid out the bear case with brutal clarity. It goes something like this:

“Eventually memory prices collapse. The Chinese will see to that. Just off what peak? And to what floor? The cost of adding capacity at these prices is no-brainer ROI. Last person in on that is fucked. And when prices squeeze, it’s economically disruptive for everyone.”

The logic is commodity 101:

Supply can expand: If oligopolies choose to add capacity, they will. CXMT (the Chinese producer) has already expanded from 120K wafers/month to 160K+, targeting 200K by year-end. State backing allows expansion regardless of profitability—the same dynamic that displaced Japan from memory leadership in the 1980s.

Demand elasticity matters: Not everyone in the memory demand space cares about hyperscale investment dynamics. When DRAM prices rise, consumer and PC/server buyers simply stop purchasing. That demand shifts elsewhere. The squeeze subsides, new capacity arrives, and the cycle repeats.

Historical patterns: DRAM upcycles typically last 18-24 months before sharp corrections of 40% or more. Even with “gangbuster demand,” as one trader put it, “MU EPS can fall by half from here. Just because the squeeze was recently so insane in the spot market doesn’t mean it’s sustainable. -50% from here is still record prices for DRAM.”

Government intervention: If sustained pricing power continues, governments will eventually intervene. Memory is strategic infrastructure, and sustained supernormal profits tend to attract political attention.

The core bear insight: there is structural demand and shortages, but this is commodity 101. Supply can expand. Demand outside AI is elastic. The cycle always turns.

Here’s something that complicates the simple bear case: cloud service providers have begun discussing 2027 long-term agreements with memory manufacturers. Even more striking, Meta and Google are reportedly negotiating 5-year LTAs with Samsung.

Think about what that means. These are the most sophisticated technology buyers on the planet—companies with dedicated supply chain teams, deep market intelligence, and zero tolerance for overpaying. And they’re locking in memory supply through 2029-2030.

Why would they do that if they expected prices to collapse?

The LTA trend signals that hyperscalers believe memory tightness is structural, not cyclical. They’re willing to sacrifice optionality—the ability to buy cheaper later—for supply certainty now. That’s a bet that the AI buildout will sustain memory demand at levels that keep prices elevated for years, not quarters.

For memory suppliers, LTAs provide revenue visibility that commodity businesses rarely enjoy. They also shift negotiating dynamics: once a hyperscaler commits to multi-year volumes at agreed pricing, they have less incentive to pressure suppliers on incremental orders.

Micron’s results have direct implications for NVIDIA’s supply chain and, by extension, the entire AI infrastructure buildout.

Every Blackwell B200 and GB200 requires HBM3E memory—Micron’s sweet spot right now. Mehrotra confirmed on the call that Micron’s HBM3E is designed into NVIDIA’s Blackwell platform, and they’ve commenced shipments to multiple large HBM customers (NVIDIA being the obvious anchor).

Here’s the critical dynamic: HBM supply constrains GPU production. NVIDIA can design the most advanced AI chips in the world, but if Samsung, SK Hynix, and Micron can’t produce enough HBM to stack on those chips, NVIDIA can’t ship. The memory suppliers have become gating factors on AI infrastructure deployment.

This creates an interesting tension. NVIDIA needs memory suppliers to expand capacity. Memory suppliers remember 2022—when they expanded into a collapsing market and took billions in writedowns. They’re being disciplined now, which benefits their margins but constrains NVIDIA’s ability to meet hyperscaler demand.

The LTA discussions suggest a potential resolution: hyperscalers committing to multi-year volumes gives memory suppliers the confidence to invest in capacity without fearing a repeat of 2022. It’s a coordination problem being solved through long-term contracts rather than spot market dynamics.

For investors, this means NVIDIA’s revenue trajectory is partially dependent on memory supplier capex decisions. If Micron, Samsung, and SK Hynix remain disciplined on capacity, NVIDIA’s growth ceiling is lower but memory margins stay elevated. If they expand aggressively, NVIDIA can ship more units but memory pricing power erodes.

Having scaled Deco Lighting from startup to $50M+ in revenue, I’ve lived through enough commodity cycles in LEDs to know both sides of this argument have merit. The truth, as usual, is nuanced.

The HBM/AI thesis is real—but the valuation question is nuanced. After today’s print, Micron trades at roughly 8-10x forward earnings on FY26 estimates—remarkably cheap if this earnings power is sustainable. Q2 guidance alone implies a $32+ annualized EPS run rate. The stock is up 176% YTD, but the multiple has actually compressed as earnings have outpaced the stock.

The cycle will turn—eventually. The question is when, and from what level. Morgan Stanley expects “the AI music to keep playing through CY26 and likely CY27, even with some skepticism CY28-30.” That’s a longer runway than bears are pricing, but it’s not infinity.

The quality of the business has genuinely improved. Exiting Crucial, the HBM technology moat, the capacity discipline—these are structural improvements. When the cycle does turn, Micron will be a different company than in 2022.

China is the wild card. CXMT’s expansion is real. But they’re still focused on DDR4/DDR5, not HBM. The technology gap in high-bandwidth memory is substantial. Whether that gap closes or widens over the next 2-3 years will largely determine how this cycle plays out.

For readers following my work on optical interconnects and datacenter infrastructure, Micron’s results fit the pattern we’ve been tracking. The AI buildout is creating pricing power across the entire stack:

Optical transceivers (Lumentum, Coherent) are seeing similar dynamics—800G is sold out, 1.6T is ramping. Power infrastructure (Bloom Energy, Vertiv) can’t build fast enough. And memory—the component that feeds every GPU cycle—is seeing the most dramatic repricing of all.

The common thread: AI workloads are so hungry for bandwidth, power, and memory that traditional supply/demand economics are breaking down. Premium products command premium prices because there simply aren’t alternatives.

Whether that persists through 2027 or collapses in 2026 is the trillion-dollar question.

Ben Pouladian is a Los Angeles-based tech investor and entrepreneur focused on AI infrastructure, semiconductors, an

d the power systems enabling the next generation of compute. He was co-founder of Deco Lighting (2005–2019), where he helped build one of the leading commercial LED lighting manufacturers in North America. Ben holds an electrical engineering degree from UC San Diego and has spent two decades building and investing in technology companies.

He currently serves on the Terasaki Institute Leadership Board and is a member of YPO (Young Presidents’ Organization). His investment research focuses on AI datacenter infrastructure, GPU computing, and the semiconductor supply chain.

Follow on Twitter/X: @benitoz More at benpouladian.com

Disclaimer: I may hold positions in securities mentioned. This is not investment advice.

Originally published on BEP Research on Substack. Subscribe for more.

Leave a Reply